<script async src="//pagead2.googlesyndication.com/pagead/js/adsbygoogle.js"></script>

<script>

(adsbygoogle = window.adsbygoogle || []).push({

google_ad_client: "ca-pub-4782552145225059",

enable_page_level_ads: true

});

</script>

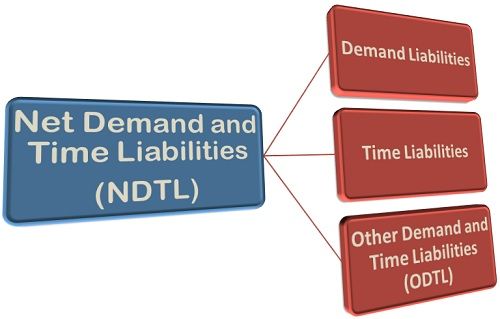

NET Demand and Time Liabilities

Bank’s NDTL = Demand and time liabilities (deposits) – deposits with other banks

Suppose a bank has deposited 5000 with the other bank and its total demand and time liabilities (including the other bank deposit) is 10,000. Then the net demand and time liabilities will be 5,000 (10,000-5,000).

Thus, the deposits of a bank are its liabilities that can be in the form of demand liability, time liability and other demand and time liabilities. Let’s discuss these in detail:

Demand Liabilities: The demand liabilities include all those liabilities of a bank which are payable on demand. Such as current deposits, cash certificates and cumulative/recurring deposits, outstanding telegraphic transfers, Demand drafts, margins against the letter of credit/guarantees, credit balance in cash credit account, etc., all are paid on demand.

Time Liabilities: Time liabilities are those liabilities of a bank which are payable otherwise on demand. These include fixed deposits, cash certificates, staff security deposits, time liabilities portion of saving deposits account, margin held against the letter of credit (if not payable on demand), gold deposits, etc.

Other Demand and Time Liabilities: These include all those miscellaneous liabilities which are not covered in above two types of liabilities. Such as interest accrued on deposits, unpaid dividend, suspense account balances showing the amount due to other banks or public, participation certificates issued to other banks, cash collaterals, etc.

C.A.S.A. ( CURRENT ACCOUNT AND SAVING ACCOUNT )

Savings Accounts

- A savings account is designed with the primary purpose to help you save.

- This type of account allows the holder to deposit money as is convenient, on which the holder can earn interest.

- A Savings account may be opened by an individual or jointly and requires the holder to usually maintain a pre-specified amount as minimum balance.

- Interest rates earned on Savings Accounts range anywhere between 4% to 6%. These accounts do usually carry the facility of issuing cheques.

Current Accounts

- Current Accounts derive their name from the purpose they are suited for, regular transactions.

- This type of account is more suited for users like firms, companies, public enterprises, businessmen, etc.

- Currents accounts do not earn any interest due to the fluidity they offer.

- Current accounts usually do not carry a limit on the number of transactions which can be made.

Savings Account v/s Current Account

A Savings account differs from a Current account in many ways and aspects. Both these accounts address different financial needs of the user, helping in better money management. Here are some of the major points based on which one can distinguish between a Savings and a Current Account.Purpose

Savings Account: A Savings Account has been designed to encourage and promote savingsCurrent Account: Is designed to facilitate regular or frequent transactions.

Ideal For

Savings account : ideal choice for any individual who earns a steady or regular income like salaried employees. This type of account is also ideal for those who have any short term financial goals to meet like a future vacation, financing a wedding, buying a car etc.current account : Is more suited individuals who are required to carry out frequent money transfers like businessmen, firms, companies, organizations, public enterprises, etc.

Monthly Transactions

Savings Account: Banks offering the facility of a Savings account do usually put a limit on the maximum number of transactions which a holder can carry out in a month. The permissible limit without attracting any charge is usually anywhere between 3 to 5 transactions per month (financial and non-financial).Current accounts: Do not have any limit on the maximum number of transactions which one can carry out. This is primarily because Current accounts serve the purpose of carrying out frequent transactions.

Interest

Savings Account: Will usually earn you an interest between 4% to 6% on a pre-specified basis. Since these accounts do not allow unlimited transactions, it is easier to accumulate more funds over a period of time.Current Account: In the case of current accounts, banks usually do not provide any interest. This is due to the fluid nature of the account which allows frequent transactions.

Minimum Balance

Minimum balance is the minimum amount of money which must always be in your account in order to prevent it from de-activating or lapsing.For Savings accounts, the minimum balance required is usually low. However, for Current accounts, one may need to maintain a relatively higher amount as minimum balance.

RECCUING AND FIXED ACCOUNT

Major Difference Between FD and RD

When we talk about RD and FD, there is one single important difference that you must be aware of, before we talk about other differentiating points. While both RD and FD runs over a tenure, FD investors can deposit an amount once while RD investors must deposit a fixed amount at regular intervals.Fixed Deposit

- Customers who opt for fixed deposits will have to choose a tenure, which usually ranges from 7 days to 10 years, and must deposit an amount once. The interest on the amount will be credited to the investor’s account on a monthly or a quarterly basis.

- When it comes to recurring deposits, investors can deposit a fixed amount every month and can earn interests. The interest is paid along with the capital at maturity.

Recurring Deposit vs Fixed Deposit

| Features / Scheme | Fixed Deposit | Recurring Deposit | ||

|---|---|---|---|---|

| Tenure | Usually, for FD schemes, the tenure ranges between 7 days to 10 years. The investor can choose a tenure that he is most comfortable with. | Tenure for Recurring deposits usually vary from 1 year to 10 years. The customer has to deposit a fixed amount at regular intervals over the tenure. | ||

| Investment Limit | There is no limit on the amount that can be invested in a fixed deposit scheme. But, this limit generally depends on the bank and the minimum investment is Rs. 100 and multiples while the maximum limit is Rs. 1.5 lakh. | While there is no prescribed minimum or maximum limit, this usually depends on the bank. Many banks have the minimum investment limit as Rs. 1000 and and the maximum limit as Rs. 15 lakhs per month. | ||

| Rate of Return | For a period of an year, the interest rate varies between 6.96% to 8.00%. The interest rate depends on the capital and tenure opted for. The interest rate for FD is slightly higher than that of RD. | The interest rate varies between 5.25% to 7.90% for a tenure of one year. The rate of interest usually depends on tenure and monthly investment amount. | ||

| Tax benefits | For fixed deposit, a tax exemption under the section 80C of Income Tax Act 1961 is applicable. | Income tax will be not deducted if the interest you earn on your rd is up to Rs.10,000. | ||

| Documents Required | Identity Proof and address proof. Customers will have to submit documents like PAN card, passport and income documents, if required. | Address proof and Identity Proof. Investors will have to submit documents like PAN card, passport and income documents, if required. | ||

| Income Interest | Interest earned on your FD is taxable and most of the banks deduct TDS. | Interest earned on your RD is taxable and most banks do not have the facility of TDS. | ||

| Additional Benefits | Loan Facility | |||

| Eligibility |

|

|||

| Withdrawal | At the end of tenure. Premature withdrawal is allowed with penalty. | At the end of opted tenure. Premature withdrawal is allowed with penalty. |

No comments:

Post a Comment