Introduction:

The automatic teller machine (ATM) is an

automatic banking machine (ABM) which allows customer to complete basic

transactions without any help of bank representatives. There are two

types of automatic teller machines (ATMs). The basic one allows the

customer to only draw cash and receive a report of the account balance.

Another one is a more complex machine which accepts the deposit,

provides credit card payment facilities and reports account information.

It is an electronic device which is used

by only bank customers to process account transactions. The users

access their account through special type of plastic card that is

encoded with user information on a magnetic strip. The strip contains an

identification code that is transmitted to the bank’s central computer

by modem. The users insert the card into ATMs to access the account and

process their account transactions. The automatic teller machine was

invented by john shepherd-Barron in year of 1960.

Automatic Telling Machine Block Diagram:

The Automatic telling machine consists of mainly two input devices and four output devices that are;Input Devices:

- Card reader

- Keypad

- Speaker

- Display Screen

- Receipt Printer

- Cash Depositor

- Card Reader:

The card reader is an input device that

reads data from a card .The card reader is part of the identification of

your particular account number and the magnetic strip on the back side

of the ATM card is used for connection with the card reader. The card is

swiped or pressed on the card reader which captures your account

information i.e. the data from the card is passed on the host processor

(server). The host processor thus uses this data to get the information

from the card holders.

- Keypad:

The card is recognized after the machine

asks further details like your personal identification number,

withdrawal and your balance enquiry Each card has a unique PIN number so

that there is little chance for some else to withdraw money from your

account. There are separate laws to protect the PIN code while sending

it to host processor. The PIN number is mostly sent in encrypted from.

The key board contains 48 keys and is interfaced to the processor.

- Speaker:

- Display Screen:

- Receipt Printer:

The receipt printer print all the

details recording your withdrawal, date and time and the amount of

withdrawn and also shows balance of your account in the receipt.

- Cash Dispenser:

The cash dispenser is a heart of the ATM. This is a central system

of the ATM machine from where the required money is obtained. From this

portion the user can collect the money. The duty of the cash dispenser

is to count each bill and give the required amount. If in some cases the

money is folded, it will be moved another section and becomes the

reject bit. All these actions are carried out by high precision sensors.

A complete record of each transaction is kept by the ATM machine with

help of an RTC device.

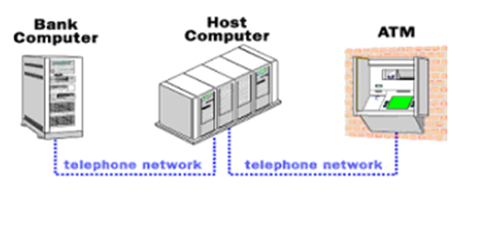

ATM Networking:

The internet service provider (ISP) also

plays an important role in the ATMs. This provides communication

between ATM and host processors. When the transaction is made, the

details are input by the card holder. This information is passed on to

the host processor by the ATM machine. The host processor checks these

details with authorized bank. If the details are matched, the host

processor sends the approval code to the ATM machine so that the cash

can be transferred.

2 Types of ATM Machines

- Leased line ATM machines

- Dial up ATM machines

The leased line machines connect direct

to the host processor through a four wire point to point dedicated

telephone line. These types of machines are preferred in place. The

operating cost of these machines is very high.

Dial Up ATM Machines:

The dial up ATMs connects to the host

processor through a normal phone line using a modem. These require a

normal connections their and their initial installation cost is very

less. The operating cost of these machines is low compared with leased

line machines.

ATM Security:

The ATM card is secured with PIN number

which is kept secret. There is no way to get the PIN number from your

card. It is encrypted by the strong software like Triple data Encryption

Slandered.

Automatic Teller Machine Working Principle:

The Automatic teller machine is simply a

data terminal with two input and four output devices. These devices are

interfaced to the processor. The processor is heart of the ATM machine.

All the ATM machines working around the world are based on centralized database system.

The ATM has to connect and communicate with the host processor

(server). The host processor is communicating with the internet service

provider (ISP). It is the gateway through all the ATM networks

available to the card holder.

When a card holder wants does an ATM

transaction, user provides necessary information through card reader and

keypad. The ATM forwards this information to the host processor. The

host processor enters the transaction request to the cardholder bank. If

the card holder requests the cash, the host processor takes the cash

from the card holder account. Once the funds are transferred from the

customer account to host processor bank account, the processor sends

approval code to the ATM and the authorized machine to dispense the

cash. This is the way to get the amount on ATMs. The ATM network is

fully based on centralized database environment. This will make life

easer and secured the cash.

Advantages of Automatic Teller Machine:

- The ATM provides 24 hours service

- The ATM provides privacy in banking communications

- The ATMs reduce the work load banks staff

- The ATM may give customer new currency notes

- The ATMs are convenient to banks customers

- The ATM is very beneficial for travelers

- The ATM provide services without any error

Features of Automatic Teller Machine:

- Transfer funds between linked bank accounts

- Receive account balance

- Prints recent transactions list

- Change your pin

- Deposit your cash

- Prepaid mobile recharge

- Bill payments

- Cash withdrawal

- Perform a range of feature in your foreign language.

⏩White Label ATM - Provided by NBFC

⏩Green Label ATM - Provided for Agricultural Transaction

⏩Orange Label ATM - Provided for Share Transactions

⏩Yellow Label ATM - provided for E-commerce

⏩PINK label ATM- women banking

⏩BROWN label ATM - ATM are those Automated Teller Machines where hardware and the lease of the ATM machine is owned by a service provider--but cash management and connectivity to banking networks is provided by a sponsor bank.

Location

ATMs can be placed at any location but are most often placed near or inside banks, shopping centers/malls, airports, railway stations, metro stations, grocery stores, petrol/gas stations, restaurants, and other locations. ATMs are also found on cruise ships and on some US Navy ships, where sailors can draw out their pay.ATMs may be on- and off-premises. On-premises ATMs are typically more advanced, multi-function machines that complement a bank branch's capabilities, and are thus more expensive. Off-premises machines are deployed by financial institutions and Independent Sales Organisations (ISOs) where there is a simple need for cash, so they are generally cheaper single function devices.

In the US, Canada and some Gulf countries, banks may have drive-thru lanes providing access to ATMs using an automobile.

In recent times, countries like India and some countries in Africa are installing ATMs in rural areas, which are solar powered.

Before an ATM is placed in a public place, it typically has undergone extensive testing with both test money and the backend computer systems that allow it to perform transactions. Banking customers also have come to expect high reliability in their ATMs, which provides incentives to ATM providers to minimise machine and network failures. Financial consequences of incorrect machine operation also provide high degrees of incentive to minimise malfunctions.

ATMs and the supporting electronic financial networks are generally very reliable, with industry benchmarks typically producing 98.25% customer availability for ATMs and up to 99.999% availability for host systems that manage the networks of ATMs. If ATM networks do go out of service, customers could be left without the ability to make transactions until the beginning of their bank's next time of opening hours.

This said, not all errors are to the detriment of customers; there have been cases of machines giving out money without debiting the account, or giving out higher value notes as a result of incorrect denomination of banknote being loaded in the money cassettes. The result of receiving too much money may be influenced by the card holder agreement in place between the customer and the bank.

Errors that can occur may be mechanical (such as card transport mechanisms; keypads; hard disk failures; envelope deposit mechanisms); software (such as operating system; device driver; application); communications; or purely down to operator error.

To aid in reliability, some ATMs print each transaction to a roll-paper journal that is stored inside the ATM, which allows its users and the related financial institutions to settle things based on the records in the journal in case there is a dispute. In some cases, transactions are posted to an electronic journal to remove the cost of supplying journal paper to the ATM and for more convenient searching of data.

Improper money checking can cause the possibility of a customer receiving counterfeit banknotes from an ATM. While bank personnel are generally trained better at spotting and removing counterfeit cash, the resulting ATM money supplies used by banks provide no guarantee for proper banknotes, as the Federal Criminal Police Office of Germany has confirmed that there are regularly incidents of false banknotes having been dispensed through ATMs. Some ATMs may be stocked and wholly owned by outside companies, which can further complicate this problem. Bill validation technology can be used by ATM providers to help ensure the authenticity of the cash before it is stocked in the machine; those with cash recycling capabilities include this capability.

Major

banks, such as HDFC Bank Ltd, Kotak Mahindra Bank Ltd and Federal Bank

Ltd, recently sent out SMSs asking some customers to change the personal

identification number (PIN) of their debit cards immediately. An SMS

from a private bank to one such customer read, “With the spike in

fraudulent transactions at ATMs in banks, your debit card ending XXXX

could have been compromised. To protect your account, we advise you to

change your PIN immediately. You can change your PIN via Net Banking,

Mobile Banking or at an ATM.”

Banks we spoke to said that this

was a precautionary measure and no breach was reported on their part.

Puneet Kapoor, senior executive vice-president, Kotak Mahindra Bank,

said, “The National Payments Corporation of India (NPCI) had alerted

that a particular network may have been compromised. In this suspected

duration, customers whose cards were used through this particular

channel, were alerted through a direct communication.” Here’s a look at

different kinds of ATM frauds out there.Fraudulent transactions

Instances like these put the focus back on security of ATM cards and their usage. Types of frauds include skimming, cloning and data theft.Skimming and cloning: Bankers and security experts state that this is the most widely known form of fraud at ATMs. A card reader, which can extract all the information from the magnetic strip present on cards, is installed in the slot where you dip your card. A hacker will then transfer this information on to a duplicate card. In some cases, you will also find a fake keypad placed above the actual keypad. Once you enter the PIN, the machine will not show any response, making a user think that the system is malfunctioning. However, the fake keypad would have copied the PIN you had entered.

Data theft: Data theft is a common way to con, especially at open ATM installation areas such as malls and shopping complexes where a person standing behind could try to distract you after you enter the PIN. Frauds also take place at point of sale (PoS) terminals, where payments are made to make a purchase. Experts say that such frauds can take place at restaurants, shops and other merchant outlets.

What can be done to prevent such frauds

The first step to protect yourself from any frauds is precautions. Opt to upgrade your card to a chip-based one, as it has added layers of safety. “Information in chip-based cards is encrypted. With a chip and PIN, card information is not validated by bank servers unless a correct PIN is used, whereas information on a magnetic strip is easily accessible,” said Amit Jaju, executive director—fraud investigation and dispute services, EY.Experts also recommend changing your PIN every 6 months. While using your card at ATMs or PoS terminals, enter your PIN carefully.

You can also limit the daily withdrawal amount on the debit card by informing your bank. If you feel that you may be a victim of such frauds, contact your bank immediately.

Banks accept liability for some frauds, not all. For instance, the bank will be liable if there was a failure of its systems and infrastructure, resulting in the fraud. But, a customer may have to share liability if there was negligence on her part.

Different Types of ATM’s

🔽

⏩On site ATM -within the premises of bank

⏩Off site ATM - Outside the bank premises

⏩Worksite ATM-Is located within the premises of an organization and is generally meant only for the employees of the organization.

⏩Cash Dispenser-Allows only cash withdrawals, balance enquiry and mini statement requests, cash dispenser(CD)

⏩Mobile ATM- refers to an ATM that moves in various areas for the customers. Few private banks have introduced ATM on wheels.

No comments:

Post a Comment